Long-Term Financial Planning for New Parents: Retirement, 529s, and Savings

College Planning Insights Young ProfessionalBrennan McCarthy, CFP®

Having a baby changes your finances in ways you feel immediately. If you’ve been tracking through the prior parts of the Expecting Parents series, you understand the importance of planning for major expenses (like daycare), major income adjustments (Minnesota’s PFML), protecting your family (insurance and estate plans), and managing your tax bill. Those decisions in the first months can shape your family's financial picture for decades.

After the adrenaline of the first few months of sleepless nights starts to wear off, it’s important to start thinking about your long-term financial path.

Here's a practical framework for new parents thinking beyond the immediate expenses.

How much Emergency Fund do New Parents Need?

Before a baby, a solid emergency fund typically means three to six months of living expenses. After a baby, that target will almost certainly be higher. Your expenses are now higher, your life is less predictable, and the cost of a financial disruption (a job loss, a medical bill, a broken furnace) is much harder to absorb when you have a child depending on you.

As I mentioned in the first part of the series on planning for daycare, automating a savings plan to tuck away $1,500/month as soon as you find out you’re pregnant not only prepares you for that expense when baby is born, but it also bolsters the emergency fund. And if your emergency fund took a hit during pregnancy or delivery, rebuilding it should be near the top of your priority list.

Protect your Own Retirement First

This may be the most important principle to keep in mind when it comes to finances: do not sacrifice your retirement savings for your children's financial future. It feels counterintuitive since we would do anything for our children, but the math is clear — your kids can borrow for college. You cannot borrow for retirement. You can save for your own retirement, or force your kids to fund it for you when you run out of money later in life.

If you've been contributing to a 401(k) or IRA, keep contributing. Make sure you’re getting at least your employer match. Beyond that, saving into a Roth IRA or a brokerage account (or a combination of the two) will make a huge impact over the long run. The compounding advantage of dollars invested in your 30s versus your 50s is significant. Protecting that is one of the best financial gifts you can give your family.

What are the Best Savings Account Options for Kids?

Once your own retirement savings are on track, you can think about building for your children. There are several account types worth understanding:

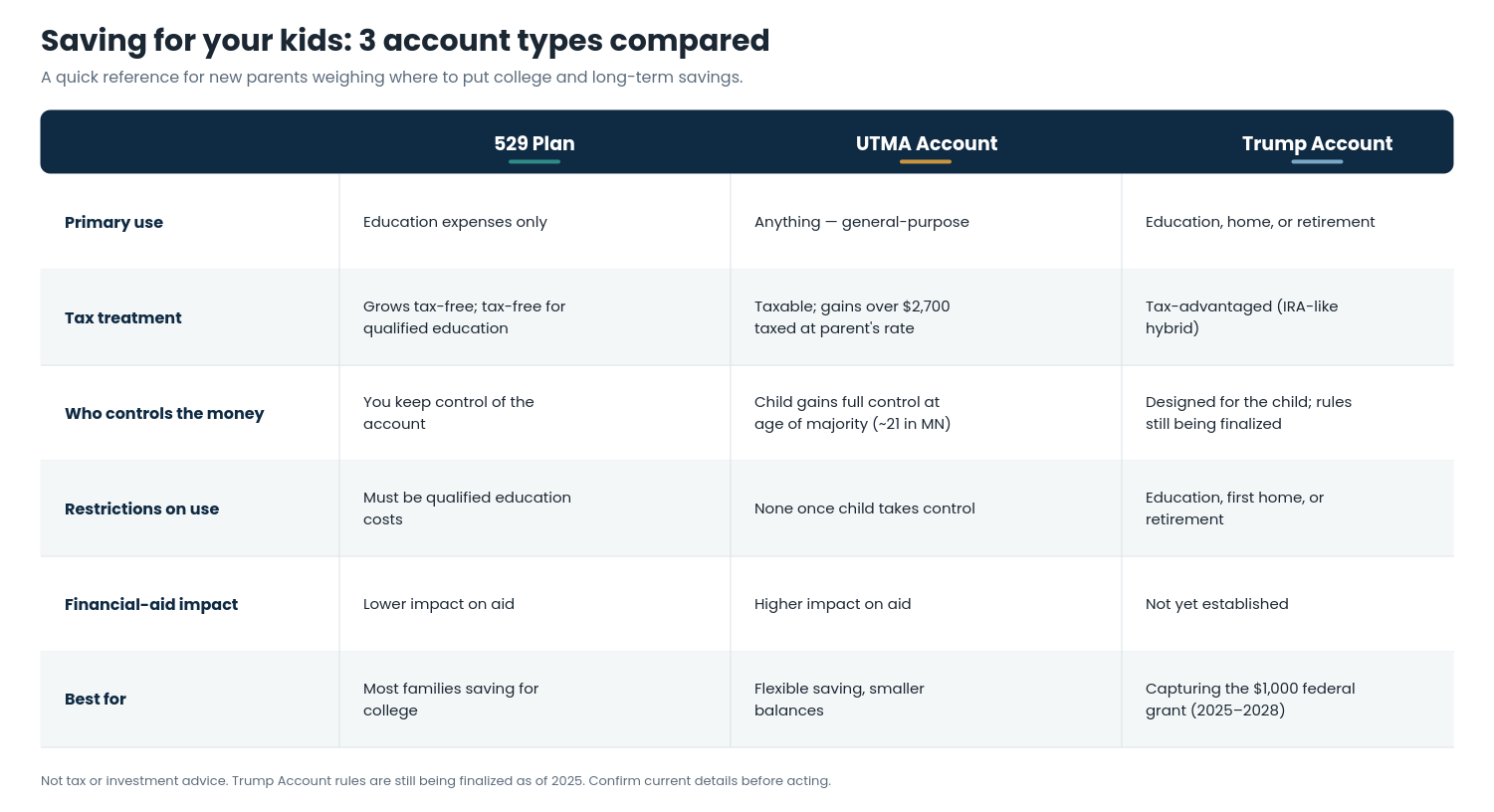

What is a 529 plan and how does it work?

A 529 is a tax-advantaged account designed for education expenses. These are the most common accounts we set up for new parents, but it’s important to understand that the funds are restricted for education expenses.

Contributions grow tax-free, and withdrawals for qualified education costs — tuition, room and board, books — are also tax-free. You can open one at any time, and accounts can be transferred to another child if the first doesn't need it.

The biggest concern some parents had in the past with opening a 529 account is the risk of saving in the account, only to have the child not end up going to college (or getting a full ride scholarship). Recent federal law changes curtail those concerns, and now allow up to $35,000 in unused 529 funds to be rolled into a Roth IRA for the child.

What is an UTMA account and what are the Tradeoffs?

An UTMA is a custodial investment account you manage on behalf of your child until they reach the age of majority (typically 21 in Minnesota). Unlike a 529, there are no restrictions on what the money can be used for — it's a general-purpose investment account.

The tradeoff is once your child reaches the age of majority, the money is legally theirs to do with as they choose. So we often open accounts like this for children, but caution parents against putting too much money into them. Most parents don’t want their 21-year old to receive tens of thousands of dollars with no strings attached. UTMAs can impact financial aid eligibility more than 529s do, so they're worth weighing carefully. It’s also important to keep in mind that a child who has more than $2,700 of unearned income (think dividends, capital gains, etc.) will get penalized by being taxed at their parents tax rate.

What are Trump Accounts and Should you use one?

As of 2025, Congress has introduced legislation to create federally seeded savings accounts for children born between 2025 and 2028, with an initial $1,000 contribution from the federal government. Because these accounts are so new and details are still being finalized, I’ve helped a handful of clients open these accounts, but we have yet to see how they behave. These accounts are designed to function like a hybrid between a Traditional IRA and a Roth IRA — tax-advantaged investment accounts that children could eventually access for purposes like education, a home purchase, or retirement. At this time, we’re encouraging any parent who has a child born in 2025-2028 to sign up for the account to receive the grant money from the Federal Government, but saving any of the parents money in an account like this is low priority (put funds in 529 or UTMA before this).

How do you Set up an Automatic Savings Plan after a Baby?

The best savings plan is one that runs without requiring a monthly decision. Most new parents I work with have significantly less money in their budget for savings than they did before the child arrived. Even still, it’s important to reset a savings plan after the baby arrives, and again after daycare starts. Even if the amount available in the budget is a low number, it’s important to get in the habit of automating that saving to keep the habit.

A useful framework for new parents: automate 1% more than feels comfortable. Not so much that it strains your budget, but enough that you're growing your savings over time without having to actively decide to do so.

How should new Parents Prioritize their Finances?

While prioritizing expenses is always an important thing to do, it becomes more acute after having a child starts to pinch the budget even more. In his book I Will Teach you to Be Rich, Ramit Sethi outlines this concept perfectly when he says to "Spend extravagantly on the things you love, and cut costs mercilessly on the things you don't." In his words, if continuing to take family vacations is important to you, then find other places to cut. If driving around a nice family SUV is more important, then it may mean sacrificing the family trips, for example.

It’s important to keep eating your financial vegetables throughout everything. Maintain retirement contributions (especially if your employer matches) and maintain your emergency fund. Second, get your insurance and legal documents in place — life insurance and a will are non-negotiable when you have a child depending on you. And finally, open a 529 and start contributing even small amounts. It could make sense to explore additional vehicles like UTMAs or Trump accounts as your capacity grows.

You don't have to do all of this at once. The goal is a clear order of operations so you're making intentional decisions rather than defaulting to inaction.

How Much should you Save for your Kids Versus Yourself?

There's no universally right answer to how much to save for your kids versus yourself, or how aggressively to build a college fund versus pay down debt. What matters most is that you're making active, informed choices rather than letting the decisions make themselves. Every dollar you direct with intention is a dollar working for your family's future.