How to Protect your Family

Insights Firm Updates Young ProfessionalBrennan McCarthy, CFP®

Having a baby changes everything. It changes your budget, your lifestyle, and how you view the world. Most importantly, it changes your priorities and what is most important. That shift demands a hard look at how to protect your family, and financial planning for new parents has different priorities than others in different life stages. There are four non-negotiables once you have a child: life insurance, disability insurance, property and casualty coverage, and an estate plan.

How Much Life Insurance do New Parents Need?

In the case of two working spouses with no kids, it can be possible for somebody who lost his/her spouse to absorb the financial loss of one income. After a baby, that calculation changes completely. The math on life insurance is simple once a child enters the picture Now there's a dependent who needs daycare, housing, food, and eventually college — none of which pays for itself.

In almost every case, term life insurance is the answer. It's straightforward: you pay a fixed premium for a set period of coverage, (typically 20 or 30 years) and if you die during that term, your beneficiary receives the death benefit. In essence, you’re renting inexpensive coverage, with the intention of outliving the term and letting it expire. This is the cheapest way to cover a new major risk. For a healthy person in their 30s, a $1 million, 20-year term policy often costs less than $50 per month. The coverage is meaningful; the cost is a worthwhile tradeoff to know your family is protected. In most of these cases, the expectation is that by the time the term expires, you will have saved enough on your own to be financially independent, and no longer need the insurance.

The harder question is how much coverage you actually need. A common rule of thumb is 10–12 times your annual income, but that's a starting point, not a formula. The real answer depends on factors like your mortgage balance, how many years of income replacement your family would need, the additional costs of not having you around (think extra childcare, home responsibilities, whether the surviving spouse plans to continue working, etc.), and whether you want to factor in future education costs. It's worth running the actual numbers rather than picking a round figure and hoping for the best.

One timing note: pregnancy itself doesn't disqualify you from getting coverage, but some insurers will make you to wait until after delivery to finalize a policy. If you’re in this situation, start the process before the third trimester so there's no gap between when the baby arrives and when your coverage is in force.

When to Add a Newborn to Health Insurance (Qualifying Life Events)

A new baby is one of the most time-sensitive insurance decisions a young family faces. Many dual-income couples arrive at parenthood each covered under their own employer's health plan, which is usually the best plan for two healthy adults. A baby changes the equation entirely, and it forces a decision that's worth thinking through well before the due date: do you add the child to one plan, or consolidate the whole family onto a single plan?

The answer depends on the specifics of each employer's offerings, and the comparison is worth doing carefully. Start by requesting the premium cost for family coverage from both employers — not just employee-plus-child, but full family coverage if there's any chance a spouse might eventually move onto the same plan. Then compare deductibles, out-of-pocket maximums, network quality, and whether your preferred providers are in-network under each option. In many cases, one employer's plan is meaningfully better or cheaper than the other, and consolidating onto that plan as a family unit makes both financial and logistical sense. In other cases, it may be more cost-effective for each spouse to remain on their own plan and add the child to whichever offers the better pediatric coverage and lower out-of-pocket costs.

One timing detail that catches many new parents off guard: the birth of a child is a qualifying life event that opens a special enrollment window (usually 30 days) that allows both spouses to make changes to their coverage outside of the normal open enrollment period. That window applies not just to adding the newborn, but to switching plans, adding a spouse, or restructuring coverage entirely. This is so important, because if you miss that 30-day window, your options are largely frozen until the next open enrollment. It's worth having the comparison done in advance so that when the baby arrives, you're executing a decision you've already made instead of reacting.

Do I need Individual Disability Insurance if I have Group Coverage?

If life insurance protects against dying too soon, disability insurance protects against something statistically more likely: becoming too sick or injured to work.

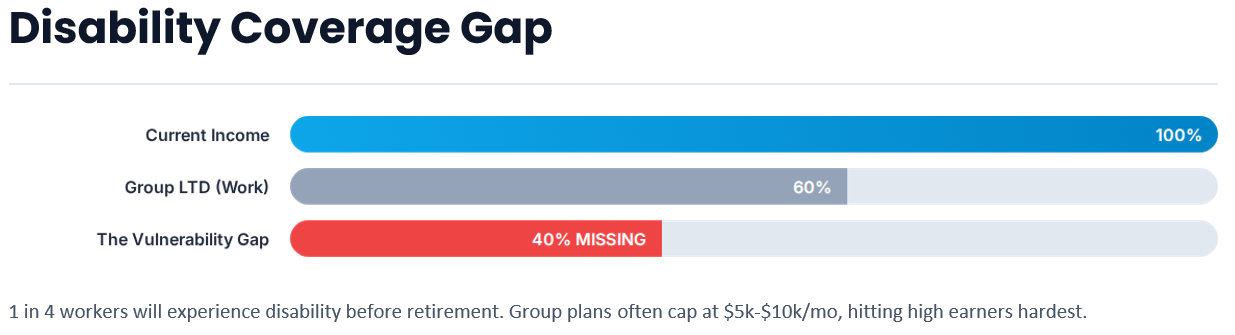

The Social Security Administration estimates that roughly one in four workers will experience a disability before reaching retirement age. For a household built built around the financial support of a high earner, a long-term disability is a huge risk that isn’t discussed enough.

Most companies offer some form of group short-term and long-term disability coverage, but the details matter enormously. Group long-term disability policies typically replace around 60% of your base salary, and they often exclude bonuses and other compensation. For a high earner, that 40% gap can be substantial. They also frequently cap monthly benefits — sometimes at $5,000 to $10,000 per month — which again hits high earners hardest.

An individual disability policy can supplement your coverage though work and fill the gap. These policies are portable (they stay with you if you change jobs), often have more favorable terms (i.e. own-occupation definition, meaning you qualify if you can't do your specific job, not just any job), and can be customized for your income level. They're more expensive than group coverage, but for a household that depends heavily on one or both professional incomes, they're usually worth paying for.

The birth of a child is also a good trigger to reassess your existing coverage. Make sure you have disability coverage through work, and if you do, understand how much it will cover if you have a catastrophic health event (like a cancer diagnosis or major injury). Do you know if that level of income replacement is sufficient in covering your families expenses if you’re unable to work?

Updating Auto, Home, and Umbrella Insurance Policies for a New Baby

This is the least glamorous part of the protection conversation, but it's worth a quick review. A few specific items to address before your due date:

Auto insurance: If you're adding a dependent, confirm your coverage limits are appropriate. I often find that young married couples have minimum liability coverage to save money. The state minimums ($30,000/person and $60,000/accident) in Minnesota for liability coverage is nowhere near enough for a family.

Homeowners insurance: Make sure you know how much coverage you have. You should have sufficient replacement cost coverage on your home (what it would cost to rebuild your home is often a higher number than what it’s worth today). A lot of carriers have reduced what they cover on roofs related to hail damage, so be sure you understand what’s covered there as well. In a lot of cases, increasing the coverage amounts can raise the price of the insurance substantially, so it’s worth looking at increasing your deductible if you can save some money on the premiums.

Umbrella policy: If you don't already have one, a personal umbrella policy is worth serious consideration once you have a child. For roughly $200–$400 per year, an umbrella policy typically adds $1 million in liability coverage above your auto and homeowners policies. It's one of the most cost-effective forms of protection available.

Essential Estate Planning Documents for Parents with Young Children

Every family with young children need to have an estate plan. The most common I see this not done by so many young couples with children is that they simply don’t think they’re going to die, so they’ll get to it later.

Having a baby eliminates "later" as an option.

At minimum, expecting parents need three documents in place before their child is born:

A will. Building a Will means getting to have the most morbid, uncomfortable conversations you may ever have. The most important feature in a will for couples with young children is addressing the Guardian – who will take care of your child(ren) if you both pass away? Without a will, that decision is left to a court. While the courts exist to prioritize the children’s best interest, the process can take a lot longer without a Will.

Additionally, all of your assets will be bestowed on your kids as soon as they reach 18 (I have yet to meet parents who are comfortable with that idea). For that reason, I always suggest parents create testamentary trusts within their will provisions – this is a trust that is created only if both parents pass away while their children are still young. The testamentary trust allows you to control the terms of passing your financial assets to the kids. In my case, my kids’ testamentary trusts say they will receive 1/3 of the assets at 25, 1/3 of the assets at 30, and the final 1/3 of assets at 35.

When you create a will, it’s also important to understand what it doesn’t cover. A will does NOT avoid probate (the assets will still go through a court process, except your will explains how you want them to pass through), and most importantly, it doesn’t override beneficiary designations on accounts.

A durable power of attorney. This designates someone to make financial decisions on your behalf if you are incapacitated. Without it, even a spouse may face legal hurdles accessing accounts or managing assets during a medical crisis.

A healthcare directive (living will). This documents your wishes for medical care if you can't speak for yourself, and designates a healthcare proxy to make decisions on your behalf.

Beyond the documents themselves, there are two administrative tasks that often get overlooked: updating beneficiary designations on retirement accounts and life insurance policies (these pass outside of your will, so a mismatch creates real problems), and confirming your child will be properly added as a beneficiary once they are born.

Financial Protection: A Necessary Evil

Insurance and Estate planning aren’t fun to think about. In the absolute best scenarios, these are tools that will incur expenses, and you’ll never receive the actual benefit of them. But when the worst happens, it’s vital that they are set up properly, and that you understand what will happen if you don’t add these pieces to your financial plan, and what makes sense to add for your family’s sake.